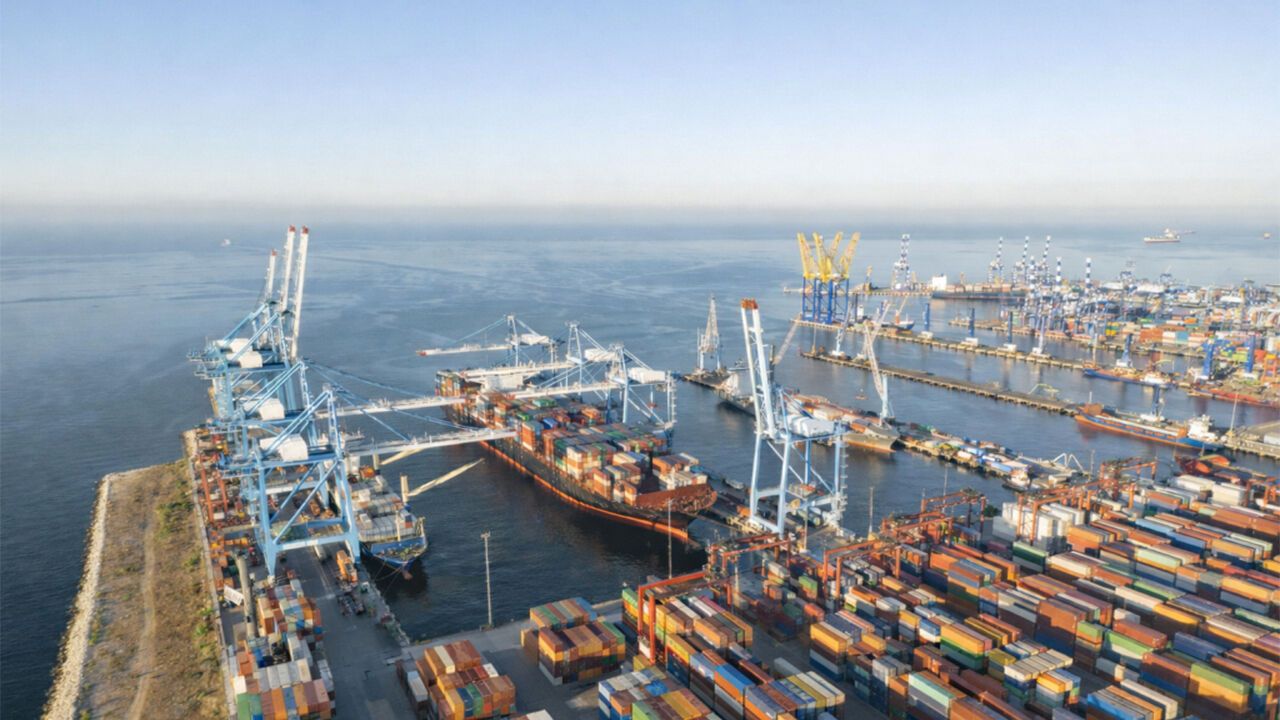

The global container freight market is being rocked again in mid-May 2026, with rates surging 12%. Drewry's weekly WCI (World Container Index), Xeneta's XSI and the Freightos Baltic Index all moved sharply higher. The main drivers are the Strait of Hormuz tanker crisis, ongoing Red Sea security threats and capacity tightening from blank sailings.

Asia–North Europe 40-foot container spot rates briefly cleared USD 4,500 while Asia–Mediterranean exceeded USD 5,200. The Asia–US West Coast leg jumped from USD 2,800 to USD 3,300 over seven days. Container-market momentum is mirroring indirect effects of the Hormuz VLCC rate spike on overall vessel deployment economics.

Carriers continue reinforcing the rally with additional blank sailings and General Rate Increase (GRI) announcements. MSC, Maersk, CMA CGM and Hapag-Lloyd announced end-May GRIs as blank sailing volumes climbed to an eight-week high through capacity withdrawal. Newbuild deliveries were expected to soften the market from March onward but the Hormuz crisis has overridden that thesis.

Supply chain takeaway: For shippers the surge hands carriers leverage in long-term contract negotiations and exposes spot-dependent cargo to cost risk. For Turkish exporters — particularly automotive, white-goods and textile firms moving raw materials and intermediate goods to Europe — the additional freight cost should be priced into Q3 contract renewals.

Key Takeaways:

1. Drewry WCI, Xeneta XSI and Freightos indices all show a 12% surge in global container freight rates in May 2026.

2. Hormuz Strait tanker crisis, Red Sea security threats and blank sailings are the main drivers of the rate spike.

3. Asia–North Europe 40-foot spot rates topped USD 4,500; Asia–Mediterranean exceeded USD 5,200.

4. MSC, Maersk, CMA CGM and Hapag-Lloyd announced end-May GRIs; blank sailing volumes hit an eight-week high.

5. Turkish exporters should price additional freight costs into Q3 contract renewals across automotive, white-goods and textile segments.