The U.S. truckload market shows no pronounced recovery signals heading into the final quarter of 2025. The Curve Report published on November 20 by freight broker RXO suggests that volumes will remain muted in the year's final quarter, though a more meaningful directional shift is possible in 2026. The Curve brand, RXO's analytics division acquired from Coyote Logistics last year, is closely monitored by the sector.

\nAccording to the report, while October and November showed relatively better performance on a year-over-year basis, this improvement has not created sustained upward pressure on spot rates. RXO expects spot prices to experience neither sharp declines nor strong gains in the near term; the market is trading within a narrow band.

\nThe report offers a notable assessment:

"Though this cycle peak may be atypical to previous — it may very well dip into deflation (without hitting a real trough) — we believe it will rise up to a more traditional peak in 2026."

This statement indicates that the current cycle is evolving differently from past truckload crises; rather than a deep collapse, the market is experiencing prolonged horizontal weakness.

Demand Problem: The Critical Issue

\nThe fundamental pressure on the market stems from demand weakness. While Bob Costello, chief economist of the American Trucking Associations (ATA), suggests that supply-side deterioration could reshape the market, academic circles emphasize that demand-side factors are more critical.

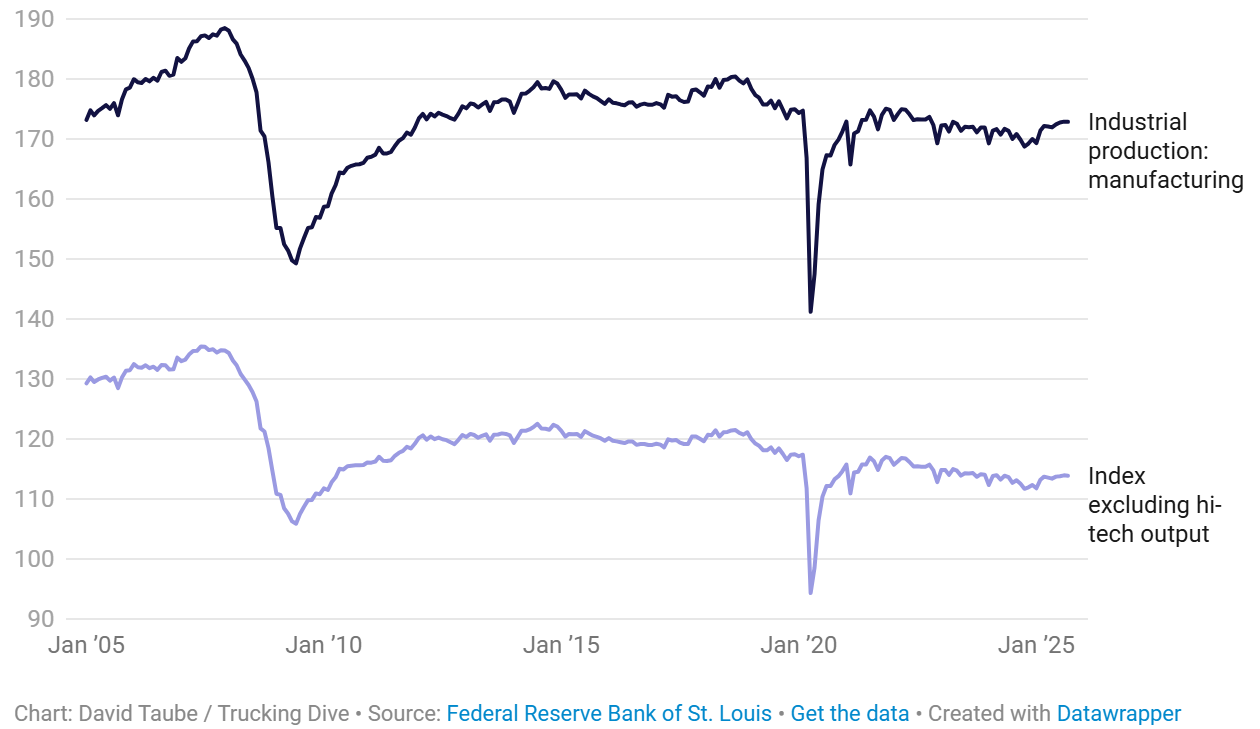

\nJason Miller, supply chain professor at Michigan State University, argues that the key to recovery in the truckload market is manufacturing output. According to Federal Reserve data:

\nU.S. manufacturing production is 7.8% below the 2007 peak.

Excluding high-technology products, this decline reaches 15.6%.

This picture demonstrates that industrial production, the primary freight source for truckload carriers, remains structurally weak.

\nPMI Indicators: Volatile and Uncertain

\nThe RXO report highlights Manufacturing Purchasing Managers' Index (PMI) data. The New Orders component is regarded as one of the strongest leading indicators for U.S. economic activity.

\nThe PMI New Orders index showed improvement for five consecutive months before declining in July.

\n Though it returned to expansion territory in August, it weakened again in subsequent months.

\n November PMI data shows new orders in contraction for the third consecutive month.

\n

In November, only the primary metals segment stood out as one of the few product groups recording growth. This underscores that truckload demand is showing only very limited sectoral improvement.

\nRate Cuts: A Source of Hope for 2026

\nDespite the weak manufacturing outlook, some supportive factors are emerging. The Federal Reserve cut the federal funds rate by 25 basis points in December, marking the third rate cut of 2025. The Federal Open Market Committee (FOMC) noted that economic activity is improving at a moderate pace, while emphasizing that uncertainty remains elevated.

\nAccording to RXO, if rate cuts continue:

\ncompanies' cost of capital could decline,

manufacturing investment could accelerate,

\n the PMI New Orders index could turn upward again.

This scenario is viewed as the foundation for truckload demand showing gradual improvement throughout 2026.

\nPolicy and Regulatory Headwinds

\nThe report identifies additional market-pressuring factors beyond demand weakness:

\n- \n

Tariff-fueled trade policy uncertainties (particularly on the U.S.–Canada corridor),

\n non-domiciled CDL enforcement,

\n Tightening on English language proficiency requirements.

These factors create additional pressure on driver supply and cross-border transportation, complicating market equilibration.

\nOverall Assessment

\nRXO's Curve report indicates that the truckload market is displaying a weak but stable picture in Q4 2025, with the real inflection point potentially arriving in 2026 through interest-rate-supported manufacturing recovery. Rather than a deep crisis, expectations center on a return to a more traditional cycle peak following a prolonged period of horizontal weakness.

\nKey Takeaways:

\nRXO forecasts truckload volumes to remain weak through Q4 2025.

\n Spot rates are compressed within a narrow band.

\n U.S. manufacturing output is 7.8% below the 2007 peak.

\n PMI New Orders showed contraction for the third consecutive month in November.

\n Fed rate cuts are the primary source of hope for 2026 recovery.

\n Trade policy and driver regulation uncertainties are adding pressure.

----------

\n\n--------------------

\nAuthor: SedatOnat.com

\n--------------------

\n\nWe would be delighted to receive your feedback.

\nWishing you happy reading from the start.

\n