Sea-Intelligence's Sunday Spotlight report, in its 736th edition, reveals that following major alliance restructurings at the beginning of 2025, Ocean Alliance has risen to the position of clear market leader on both Transpacific and Asia–Europe routes.

\nAs the renewed route networks stabilize, analysis based on the eight-week moving average of "operated capacity market share" clearly demonstrates the global market impact of carrier alliances.

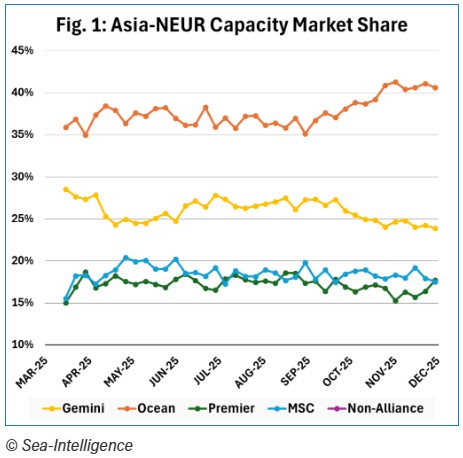

\nOcean Alliance Leads on Asia–Northern Europe Route

\nThe report shows that Ocean Alliance on the Asia–Northern Europe route is well ahead of competitors.

\nWhile the alliance's market share has long hovered in the 36–38 percent range, it is expected to exceed 39 percent in the coming months and reach 41 percent by December 2025.

This rate creates a strong gap ahead of both Gemini Cooperation and Premier Alliance.

\n- \n

Gemini Cooperation's share risks declining to 24–25 percent,

\n Premier Alliance and MSC (Mediterranean Shipping Company) are positioned in close proximity in the same segment.

\n

According to Sea-Intelligence's analysis, this trend demonstrates that Ocean Alliance's long-term Asia–Europe strategy is bearing fruit.

\nStrong Consolidation on Transpacific Route

\nA similar picture is emerging on Transpacific routes.

\n

\nOcean Alliance is expected to reach 37 percent market share on the Asia–North America West Coast route by year-end.

On the East Coast route, the share is expected to climb to the 38–40 percent range — meaning it would be approximately 20 percentage points ahead of individual competitors.

\nThis result demonstrates that Ocean Alliance optimizes container capacity, service frequency, and port connectivity far more efficiently than competing alliances.

\nCompetition Intensifying on Asia–Mediterranean Route

\nThe report notes that the Asia–Mediterranean route has a more fragmented and competitive market structure.

\nNevertheless, it is stated that Ocean Alliance has begun increasing its share here as well and is positioning itself to challenge MSC's traditional dominance.

In this region, strategic moves such as capacity reallocation among alliances and port rotation optimization are expected to intensify competition.

\nGap Between Gemini and Premier Alliance Narrowing

\nGemini Cooperation (the Maersk & Hapag-Lloyd partnership) has long held second place, but recent capacity losses have dragged the alliance's market share downward.

\n

\n Premier Alliance (a structure encompassing carriers such as Evergreen, ONE, and Yang Ming) is partially filling this gap and approaching the 20 percent range.

Sea-Intelligence analysts predict that as of 2026, the gap among the three major alliances may narrow, but Ocean Alliance will maintain its strategic advantage.

\nOcean Alliance: Strategic Power After Restructuring

\nThe alliance restructuring at the beginning of 2025 reshaped route sharing, vessel capacity allocation, and operational integration processes among carriers.

\n

\nOcean Alliance, composed of the partnership of COSCO Shipping, CMA CGM, OOCL, and Evergreen, emerged as the strongest from this process.

The alliance's leadership is built particularly on the following factors:

\n- \n

High utilization rate

\n Comprehensive port coverage

\n Rotation flexibility and low blank sailings rate

\n Asia-based cost advantage

\n

According to Sea-Intelligence, these factors have elevated Ocean Alliance to the position of "not only the largest, but also the most stable" alliance.

\nConclusion: Ocean Alliance Shapes New Balance in Global Shipping

\nFollowing the 2025 restructuring, the global container shipping map is being redrawn.

\nOcean Alliance has shifted the balance of power among alliances in its favor by establishing clear leadership on both Asia–Europe and Transpacific routes.

Gemini Cooperation and Premier Alliance are attempting to remain competitive in this new environment with more limited capacity growth.

\nThough oversupply risk and price pressure persist in the container market, Ocean Alliance is expected to maintain its market leadership thanks to economies of scale and strategic alignment.

\nKey Takeaways:

\n- \n

Ocean Alliance holds the leading position on Transpacific and Asia–Europe routes following the 2025 restructuring.

\n Its share on the Asia–Northern Europe route could climb as high as 41 percent.

\n Gemini Cooperation risks seeing its share decline to 24–25 percent.

\n On Transpacific East and West Coast routes, Ocean Alliance is approximately 20 percentage points ahead of its competitors.

\n On the Asia–Mediterranean route, MSC's leadership is weakening, and the market is becoming more competitive.

\n Coordination among COSCO, CMA CGM, OOCL, and Evergreen is pivotal to Ocean Alliance's success.

\n Analysts expect the alliance to maintain its leadership through 2026 with high capacity management, low blank sailings rate, and global reach.

\n

----------

\n\n--------------------

\n\nWe would be delighted to receive your feedback.

\nWishing you happy reading.

\n